Andrew Hallam

13.03.2020

Would The 4% Rule Work If You Retired Before A Crash?

_

Stock market fears are higher than a Coronavirus fever. Many investors worry what will happen to their hard-earned savings if stocks crash. Young investors shouldn’t worry. If stocks crash today, and they add money every month, it should juice their long-term profits.

But retirees are more afraid. After all, they aren’t accumulating assets. They’re selling them instead. Many retirees know about the 4 percent rule. If you have a low-cost, diversified portfolio, and if you withdraw an inflation-adjusted 4 percent per year, it should last at least 30 years.

The odds of the money lasting increase dramatically if you retire on the eve of a long bull run. But what if you retire right before a market crash?

The 4 percent rule was back-tested to 1926. Even if you had retired in 1929, a diversified portfolio with 60 percent U.S. stocks and 40 percent bonds would have lasted at least 30 years, if you withdrew an inflation-adjusted 4 percent per year.

But these back-tests didn’t include investment fees. Nor did they include a diversified portfolio of U.S. and international stocks. Instead, the studies only measured U.S. stocks. As a result, this unintentional cherry picking focused only on the world’s best performing market.

If you’re ready to retire, you might wonder how the 4 percent rule stacked up for those who retired before the last two major market crashes. Unlike a theoretical back-test, these investors would have paid investment fees. They should have also had diversified portfolios with U.S. and international stocks. Using portfoliovisualizer.com, I decided to have a look.

Assume someone retired in January 2000. Stocks traded at a CAPE ratio higher than 40 times earnings. In other words, stocks were more expensive then (relative to business earnings) than at any time in history. Today, U.S. stocks trade at a CAPE ratio of about 29 times earnings.

Assume they had $500,000 when they retired. Forty percent of it was in Vanguard’s Total Bond Market Index Fund (VBMFX). Another 40 percent was invested in Vanguard’s Total Stock Market Index Fund (VTSMX), comprising U.S. stocks. The remaining 20 percent was invested in Vanguard’s International Stock Market Index (VGTSX). There’s nothing strategic about this allocation. It’s diversified and simple. It also would have been effective.

But in 2000, this new retiree might have worried. After all, U.S. stocks fell about 9 percent that year. The following year, 2001, the market dropped a further 12 percent. And if that didn’t test the retiree’s mettle, U.S. stocks cratered another 22 percent in 2002.

Meanwhile, if the investor were withdrawing an inflation-adjusted 4 percent per year, they would have been selling during market lows. In 2000, the investor would have sold $20,677. They would have given themselves a raise to cover the following year’s inflation, withdrawing a further $20,998 in 2001. In 2002, they would have withdrawn an additional $21,497. And they would have continued to withdraw more money every year to keep pace with inflation.

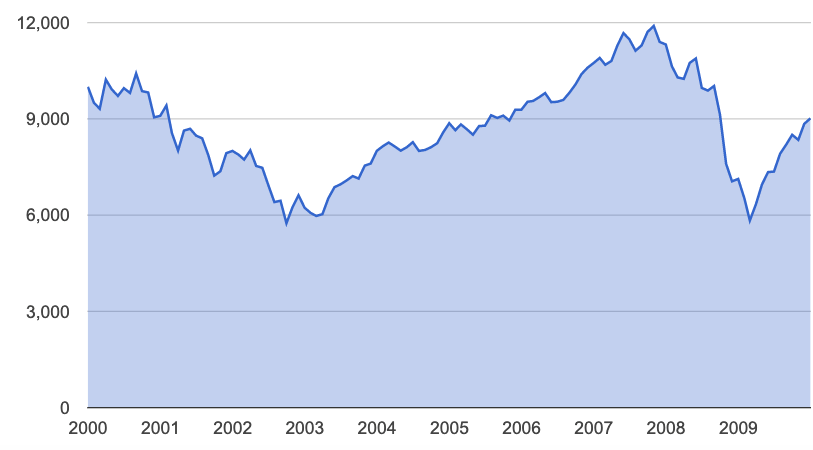

After retiring on the eve of this horrific market crash, you might wonder if the investor would have anything left today. After all, they would have withdrawn a total of $452,502. They would also have faced the “lost decade” for U.S. stocks. As shown below, if $10,000 were invested in the S&P 500 at the beginning of 2000, it would have been worth just $9,016, a full ten years later.

Source: portfoliovisualizer.com

*Vanguard’s S&P 500 Index

But despite this horrible start to their retirement, the retiree would have almost as much money today (more than 19 years later) as they did when they first retired.

To recap, they would have retired in January 2000 with $500,000. They would have withdrawn a total of $452,502 by January 2020. And by February 29, 2020, their portfolio would be worth $485,397.

How Did The 4% Rule Stack Up?

Retirement Date: January 1, 2000

Portfolio’s Beginning Value: $500,000

Total Withdrawn Over 19 Years and 2 months: $452,502

Portfolio Value (March 1, 2020): $485,397

| Year | Inflation | Return | Year-End Value | Amount Withdrawn Each Year |

|---|---|---|---|---|

| 2000 | 3.39% | -2.80% | USD 465'342 | USD -20'677 |

| 2001 | 1.55% | -5.05% | USD 420'863 | USD -20'998 |

| 2002 | 2.38% | -8.10% | USD 365'285 | USD -21'497 |

| 2003 | 1.88% | 22.20% | USD 424'473 | USD -21'901 |

| 2004 | 3.26% | 10.87% | USD 447'990 | USD -22'614 |

| 2005 | 3.42% | 6.46% | USD 453'564 | USD -23'387 |

| 2006 | 2.54% | 13.24% | USD 489'632 | USD -23'981 |

| 2007 | 4.08% | 8.07% | USD 504'179 | USD -24'960 |

| 2008 | 0.09% | -21.61% | USD 370'222 | USD -24'983 |

| 2009 | 2.72% | 21.20% | USD 423'041 | USD -25'662 |

| 2010 | 1.50% | 11.63% | USD 446'195 | USD -26'046 |

| 2011 | 2.96% | 0.50% | USD 421'586 | USD -26'818 |

| 2012 | 1.74% | 11.75% | USD 443'832 | USD -27'285 |

| 2013 | 1.50% | 15.44% | USD 484'683 | USD -27'694 |

| 2014 | 0.76% | 6.43% | USD 487'931 | USD -27'904 |

| 2015 | 0.73% | -0.64% | USD 456'711 | USD -28'108 |

| 2016 | 2.07% | 6.94% | USD 459'729 | USD -28'691 |

| 2017 | 2.11% | 15.28% | USD 500'700 | USD -29'296 |

| 2018 | 1.91% | -5.04% | USD 445'600 | USD -29'855 |

| 2019 | 2.29% | 19.99% | USD 504'130 | USD -30'538 |

| 2020 | 0.00% | -3.72% | USD 485'397 | USD 0.00 |

Source: portfoliovisualizer.com

*Returns to February 29, 2020

What about someone who retired in January 2008 with $500,000? That was another nail-biting year. U.S. stocks fell 37 percent. International stocks fell even further. If the retiree withdrew an inflation-adjusted 4 percent per year, by 2020, they would have taken a total of $266,372 from their account. And despite those withdrawals, their portfolio would be worth more today than it was when they first retired. By February 29, 2020, they would have had $577,742 remaining.

How Did The 4% Rule Stack Up?

Retirement Date: January 1, 2008

Portfolio’s Beginning Value: $500,000

Total Withdrawn Over 12 Years and 2 months: $266,372

Portfolio Value (March 1, 2020): $577,742

| Year | Inflation | Portfolio Return | Year-End Value | Amount Withdrawn Each Year |

|---|---|---|---|---|

| 2008 | 0.09% | -21.61% | USD 371'911 | USD -20'018 |

| 2009 | 2.72% | 21.20% | USD 430'186 | USD -20'563 |

| 2010 | 1.50% | 11.63% | USD 459'348 | USD -20'871 |

| 2011 | 2.96% | 0.50% | USD 440'133 | USD -21'489 |

| 2012 | 1.74% | 11.75% | USD 469'980 | USD - 21'863 |

| 2013 | 1.50% | 15.44% | USD 520'372 | USD -22'191 |

| 2014 | 0.76% | 6.43% | USD 531'458 | USD -22'359 |

| 2015 | 0.73% | -0.64% | USD 505'546 | USD -22'522 |

| 2016 | 2.07% | 6.94% | USD 517'656 | USD -22'990 |

| 2017 | 2.11% | 15.28% | USD 573'302 | USD -23'474 |

| 2018 | 1.91% | -5.04% | USD 520'474 | USD -23'923 |

| 2019 | 2.29% | 19.99% | USD 600'038 | USD -24'469 |

| 2020 | 0.00% | -3.72% | USD 577'742 | USD 0.00 |

Source: portfoliovisualizer.com

Returns to February 29, 2020

Portfolio back-tests, however, aren’t future guarantees. Investors might wonder what would happen if they retired on the eve of a 1929-like market crash, coupled with runaway inflation (such as we saw in the early 80s) and low bond market returns (such as we have today). Historically that combination has never happened. But you might ask, “What if it did?”

Vanguard’s Monte Carlo calculator helps to answer that question. This nifty tool runs more than 100,000 possible scenarios. You start by entering how long you think you’ll live and your portfolio allocation. You also enter what inflation-adjusted withdrawal rate you would like to make each year. Based on the Monte Carlo calculator, a retiree who withdraws an inflation-adjusted 4 percent per year (from a portfolio of 60 percent stocks and 40 percent bonds) has a 91 percent chance of their money lasting 30 years.

If investors can stomach higher volatility, a portfolio comprising 70 percent stocks and 30 percent bonds has a 97 percent chance of lasting 30 years.

But a retiree’s biggest risk isn’t the stock market. It’s not inflation either. Instead, it’s the person they face in the mirror each day. Retirees should do their best to channel their inner Zen. Year-to-year returns don’t matter much. Even a decade-long return (like 2000-2010) can have less impact than we think. Ignore market volatility, market forecasts and market drops. If possible (I know this isn’t easy) ignore the portfolio value too.

Stick to a solid plan and have faith that it will work. That’s easier said than done. But worrying never helps. And those who act on speculation are usually the only ones that lose.

Further Related Reading

How Retirees Can Withdraw More Than 4 Percent Per Year

Andrew Hallam is a Digital Nomad. He’s the author of the bestseller, Millionaire Teacher and Millionaire Expat: How To Build Wealth Living Overseas

Swissquote Bank Europe S.A. accepts no responsibility for the content of this report and makes no warranty as to its accuracy of completeness. This report is not intended to be financial advice, or a recommendation for any investment or investment strategy. The information is prepared for general information only, and as such, the specific needs, investment objectives or financial situation of any particular user have not been taken into consideration. Opinions expressed are those of the author, not Swissquote Bank Europe and Swissquote Bank Europe accepts no liability for any loss caused by the use of this information. This report contains information produced by a third party that has been remunerated by Swissquote Bank Europe.

Please note the value of investments can go down as well as up, and you may not get back all the money that you invest. Past performance is no guarantee of future results.